I always define my risk, and I don't have to worry about it." -- Tony Saliba

Young investors are a class apart, each of them has their own perception about money. In fact in the last one week, I found two extremes of them approaching me.

Mr Harish, in his early 20s was employed with a BPO, a well-paying job and with time in hand, he chose to dabble in stocks and saw some quick bucks coming in initially. In fact, it made him the hero in the office as he was considered the guru in stocks in his department. All was well until the markets came crashing down. He expected markets to recover quickly as in the recent past and chose to use the futures market -- the market sentiment was clearly pointing out to a rally in his view. He now sits on a whopping Rs four lakh loss, not knowing what to do!

Other Get Ahead features:

CAT: Two-week countdown

Diwali: Style of the fashionistas

BPO careers and the global financial crisis

11 ways to be a happy employee

At a seminar that I recently conducted, where we cover taxation and investments as part of an induction process, a majority of participants were just out of college. The repeated question that I was asked was: "Is there a need to invest? I am always running up credit card outstandings -- instead of investing Rs 100, I would rather have Rs 70 in hand to spend. Three years is such a long time."

These are two extreme cases within which most youngsters fall, they either dabble too much in the equities or don't invest at all! Both scenarios are not good for any investor.

To risk or not to risk?

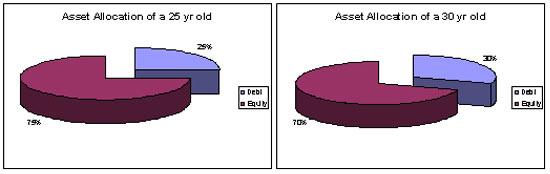

Let me start with Harish. Should he have avoided equities completely? At his age, he could definitely take risk. What is an appropriate risk level that an investor should take? How much is too much? These are concerns that every investor has. For someone who had all his investment in equities, he would have now realised that the exposure was definitely too much. A crude thumb rule is to have equity exposure of 100 -- your age + equity exposure (eg your age is 25 years, then you could have an equity exposure of 75 per cent).

It is ideal to have different forms of investments within equity and debt forms. For instance one can pick stocks directly while also investing in mutual funds. You can simultaneously use the Systematic Investment Plan (SIP) approach of monthly investments in mutual funds.

The mistake Harish made was to get carried away by the market and the initial profits. Only by experience would one realise that when markets are at a peak, the fall is round the corner! For many of us who have burnt our fingers investing the first time, learn from this experience the next time around. The other mistake made was to increase risk at peaks. This is a temptation one should resist and never take a higher risk than one can afford. Harish ran up a loss almost equal to his income for the full year. And that is not the best situation to be in.

To Invest or Not To Invest?

On the other hand one is tempted not to invest and spend in initial years. You need to invest for your future and also to reduce your taxes. A person in the 30 per cent tax bracket investing Rs 100 at an 8 per cent post tax return would get Rs 125 in three years.

On the other hand if you did not invest, your take-home would be lesser by Rs 30 and hence you can spend only Rs 70. You have lost out an opportunity to increase your money by Rs 55 over the base of Rs 70 you would have otherwise had to spend -- you have made a whole 80 per cent higher return in a short span of three years, even in a conservative investment avenue.

If you take advantage of your full limit for the initial years of your career, there is a substantial asset creation that you are building for yourself. Investments made in the initial years provide the best compounding -- so the more you invest in your initial years, the better.

Spread your investment across short-medium-long term horizons to also take care of your financial needs. Short definitely doesn't mean 'a day' or 'a week', it is a period of three-five years if you are using equity. Equities take that long to reap you best returns in line with market cycles.

Tips to get started!

- Set aside at least 20 per cent of your income towards investments as a thumb rule.

- Use the power of compounding -- the earlier you start the better.

- Have clarity on your risk/ return profile and don't overdo your equity exposure.

- Use SIPs into equity mutual funds for most part of your investments initially.

- Enter direct equities in a phased manner.

- Have some amount in debt funds as well.

- Choose your investments after good amount of research. Use this as an opportunity of learning on the practical aspects of finance.

- Learn from your mistakes. Patience and self discipline are key factors to being a successful investor.

Anil Rego is the CEO and founder of Right Horizons, an investment advisory and wealth management firm.