Get Ahead presents the TCS Smart Business Case Study Contest for young managers, along with The Smart Manager, the management magazine! We give you a profile and history of a company. All you have to do is study it and post your solution here, upto 500 words. The winning solution stands to win Rs 25,000! The Smart Manager will also publish your photograph and solution in its next issue! Hurry! The last date to post your solution is January 31.

ver the last few months, it has been widely conjectured that India's Finance Ministry has been looking around at a few profitable public sector companies (PSUs) to fund its fiscal deficits through special dividends over and much above the normally declared dividends.

ver the last few months, it has been widely conjectured that India's Finance Ministry has been looking around at a few profitable public sector companies (PSUs) to fund its fiscal deficits through special dividends over and much above the normally declared dividends.

Prominent among these PSUs are the oil and gas majors like Central Oil and Fuel Corporation (COFC) and India Energy Limited (IEL).

The government had already done a similar milking strategy earlier in 2001 with its telecom monopoly Bidesh Sanchar Corporation (BSC), before it was disinvested to the private sector. BSC shelled out Rs 22.5 billion as a special interim dividend just before its privatisation.

The argument then was that since the company was being privatised, the government was only taking out the cash which rightfully belonged to it.

The case of COFC is different.

The government is unlikely to either divest or dilute its equity in the national oil company in the foreseeable future. But it argues that the targeting of the oil companies is legitimate since these companies profited from subsidies on kerosene and domestic LPG over the years.

It was also suggested that COFC had gained the most in the de-controlled regime by getting globally benchmarked price for crude oil while its cost of capital was highly subsidised.

In recent times, this was as high as $28 (approximately Rs 1,228) per barrel instead of a fixed $16 (Rs 702) earlier. And COFC's kitty is swelling because of this distortion.

By and large, similar reasons as in the case of BSC were proffered for taking the cash out of these companies.

Milking the cash cows to pay for failures elsewhere?

The real reason for huge cash withdrawals from COFC, according to many financial pundits, is that the central government faces an acute revenue shortfall, compounded by its inability to meet the targets for disinvestments.

The revenue gap is said to be as much as Rs 100 billion out of the total disinvestment target of Rs 120 billion for the year 2004-2005.

Moreover, government expenditures are mounting due to administrative inefficiencies and overstaffing, poor performance in tax collections and increased non-plan expenditures.

As of now, no one seems to know the exact amount these national oil companies have been asked to pay.

Apparently, COFC has been asked to pay as much as Rs 60 billion to Rs 100 billion as a special dividend.

Another report suggests that the dividend payout for all oil companies has been scaled down to Rs 26 billion, out of which COFC would contribute Rs 17 billion.

About COFC

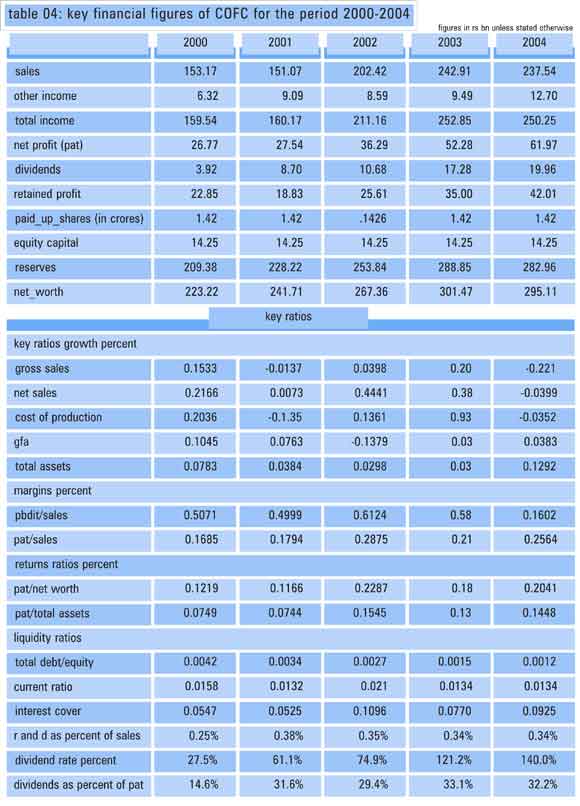

COFC, India's biggest oil exploration company, has an excellent track record in declaring dividends.

A hefty 140% dividend was announced for the year 2003-04, which was over 30% of its net profits for that year. This resulted in an outgo of Rs 19.96 billion.

In 2002-03, it had paid a 121% dividend of Rs 17.28 billion.

The company is still cash rich and has balance sheet reserves and surplus amounting to Rs 282.96 billion for the year ending March 2004.

As a result of low production costs and receiving global market prices, COFC is India's most profitable company.

For the year 2003-2004, COFC's net profit was Rs 61.98 billion, about 2.5 times more than the next most profitable company, Oil of India Corporation (OIC).

It topped the ET500 rankings in September 2004 by displacing the more regular occupants: Bharat Levers (BLL), the Globolevers subsidiary in India, and Pepro, a homegrown infotech giant.

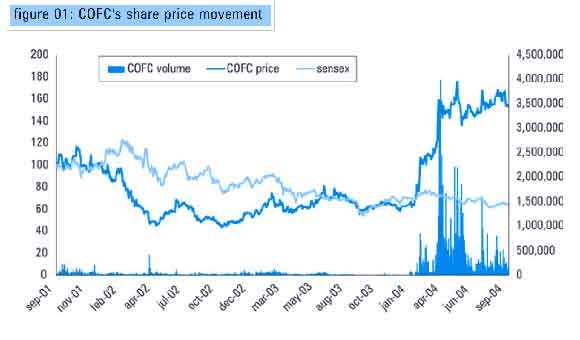

With a market capitalisation over Rs 550 billion, the company topped the Business First's BF1000 rankings in December 2004, overtaking the more famous private enterprises like Infocomm and BLL for the amount of wealth created.

COFC also outperformed the BSE Sensex during last two years.

COFC in the post-APM scenario

COFC, till recently, operated in a protected market.

It was required to sell its product, mainly crude oil, to public sector oil companies at a price that was much lower than the international prices of crude oil.

At the same time, it had privileged access to India's best oilfields. After the removal of the Administered Price Mechanism (APM), the company could sell its crude at a price determined by the international markets.

This policy change, however, also exposed it to the vagaries of international oil price fluctuations.

The company needs to expand badly, build new assets offshore and buy-in fresh assets in other countries to remain an internationally competitive corporate entity.

COFC plans to tackle the policy induced challenges in two major directions:

First, it wants to take advantage of the globalisation process and expand operations globally. Second, it will integrate itself into downstream activities like transportation, refining and marketing.

Subroto Raman, chairman and managing director, COFC, feels the business strategy of COFC should be a continued focus on its core business of exploration and production. At the same time, it should go for vertical integration to secure sustained growth.

COFC has bared such growth intentions by acquiring the 37% stake of the Rising Sun Group in the loss-making Mannur Refinery & Petrochemicals (MRPL).

Subroto Raman also wants to build a strong downstream presence by trying to acquire central government's stake in Petroleum Corporation Limited (PCL).

According to him, "We have already requested to be allowed to bid for PCL as it would help us attain vertical integration along the entire value chain of petroleum business. With the acquisition, we can go into transport fuel marketing without a long gestation period as against potential competitors who pose formidable entry barriers."

COFC also plans to enter the retail business of transport fuels by opening 600 petrol-filling stations around the country, making it a full vertically integrated oil company.

More important, these synergistic forays will also diversify the company's risks.

One of India's leading credit rating agencies commented on these strategic approaches, "It is like having a balanced portfolio with the risks evenly spread out. When crude prices spurt, COFC gains from upstream activity, and when they crash, its refining margins go up. It is win-win for COFC."

Does paying special dividend affect COFC's long term prospects?

Though COFC is now the largest company in India in terms of market capitalisation and net profits, it is already facing major competitive challenges.

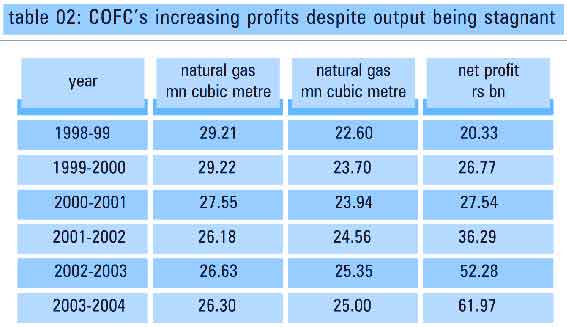

The management has realised that its high profitability is mainly due to favourable crude oil prices in the post-deregulation era.

Further, despite net profits spiralling upwards, its crude oil output has remained stagnant and even declined in the last five years.

A business writer wrote succinctly on this, "The strong bottom line can be traced to a windfall of high crude oil prices, rather than any great strides in operational efficiency. Whether global oil prices will remain high beyond the near term is the great big imponderable."

It is obvious that for COFC to remain competitive and grow rapidly, it needs to show a much higher commitment and speed in:

1. Investing in technology to upgrade its recovery and efficiency to global benchmarks, as well as invest in oilfields abroad to remain competitive in this changing scenario of global competition.

2. Improving reserve accretion to retain its growth of profits considering that now it does not have proprietary rights even in India to explore oil fields.

3. Integrating downstream to mitigate risks of oil price fluctuations and compete with global integrated oil companies.

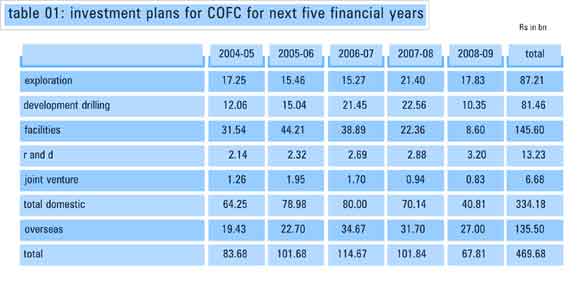

To implement the above, the management has planned huge investments aggregating to Rs 480 billion during the next five-year plan

The proposed dividend could also put a question mark over the funding of COFC's current projects, since the company has an annual capital expenditure of more than Rs 80 billion towards the redevelopment of oil wells and other investments in overseas markets during the year.

COFC requires surpluses and cash to make these massive investments.

Though COFC has over Rs 280 billion in reserves, only Rs 60 billion of it is cash reserves. It would have to pay Rs 30 billion in the current financial year itself to acquire a 25% stake in a Sudanese oil field.

This means that even to pay the proposed special dividend, COFC would have to encash some of its term deposits. Also, with a huge one-time outgo, it may be required to borrow for funding its normal capital expenditures in the following year.

Note: Debt is usually available to oil exploration companies at a high interest premium due to the inherent business risks involved.

Role of COFC's board: Can it strike a balance?

The role of a company's board in the narrow financial view is to maximize the value of shareholders' equity. A broader stakeholder view entails the board to keep the reasonable and legitimate interests of the other stakeholders in mind while taking strategic decisions like those involving expansion, closures, mergers and acquisitions.

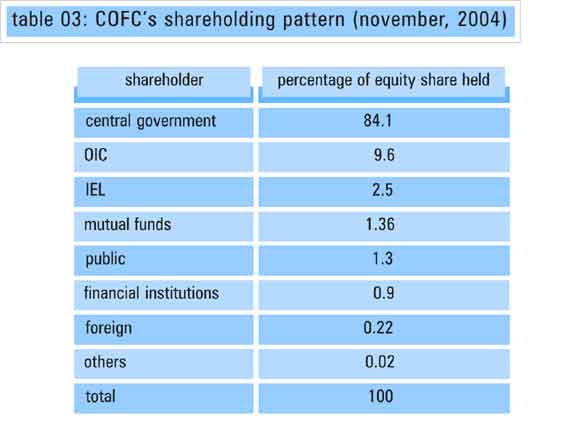

The central government is the largest shareholder in COFC with 84% equity.

Given that Oil of India Corporation (OIC) and IEL (the other major equity holders in COFC) too are government owned, the latter effectively owns 96% of the company.

A high 'special' dividend might bail out the central government from its problems of huge fiscal deficit, but it may hurt the future investment plans of COFC. It could even endanger the very survival of the company considering its internal intrinsic problems and heightened external competition.

Given this, such a move may not be in the long-term interest of the majority shareholder, that is, the government itself. In other words the government in one strike could kill the hen that lays golden eggs.

A business editor summed up the situation rightly: "The Government's proposal to 'get' COFC to declare a hefty special dividend could spell disaster not just for the company but the economy as a whole To a government hungry for cash, COFC 's coffers obviously present an inviting sight. But this is one coffer that the Government should only stare at and not covet, for at stake is not just a few crore rupees but the energy security of the country itself."

Also in this case a legitimate claim of a majority shareholder could be detrimental to the interests of other direct and indirect stakeholders, such as, the employees and the Indian economy as a whole.

Questions for you:

1. Given this background, in whose interest should the board take a decision?

2. Is the government correct in asking for special dividends from companies like COFC?

Submit your case analysis at

https://www.thesmartmanager.com/smartcase/smartcase.html

Powered by ![]()

Published with the kind permission of The Smart Manager.

Click here to avail of a special subscription offer for rediff Get Ahead readers!